A nemzetközi cégek körében egyre gyakoribb a határokon átnyúló foglalkoztatás. Ennek jogi és adózási vonzatai összetettek, érdemes előre megtervezni a folyamatok adózási és társadalombiztosítási vonzatát. Az alábbiakban a határon átnyúló foglalkoztatás három leggyakoribb esetét ismertetjük.

Egy Magyarországon dolgozó lengyel mérnök példáját alapul véve elemezzük az adó- és társadalombiztosítási következményeket és lehetőségeket, rávilágítva néhány klasszikus buktatóra is. Bár példánkban a munkavállaló lengyel állampolgár, az elemzés eredménye a más EU-országokból, például Németországból, Ausztriából, Szlovákiából, stb. érkező dolgozók esetében is hasonló. A cikk többi része angolul olvasható az alábbiakban.

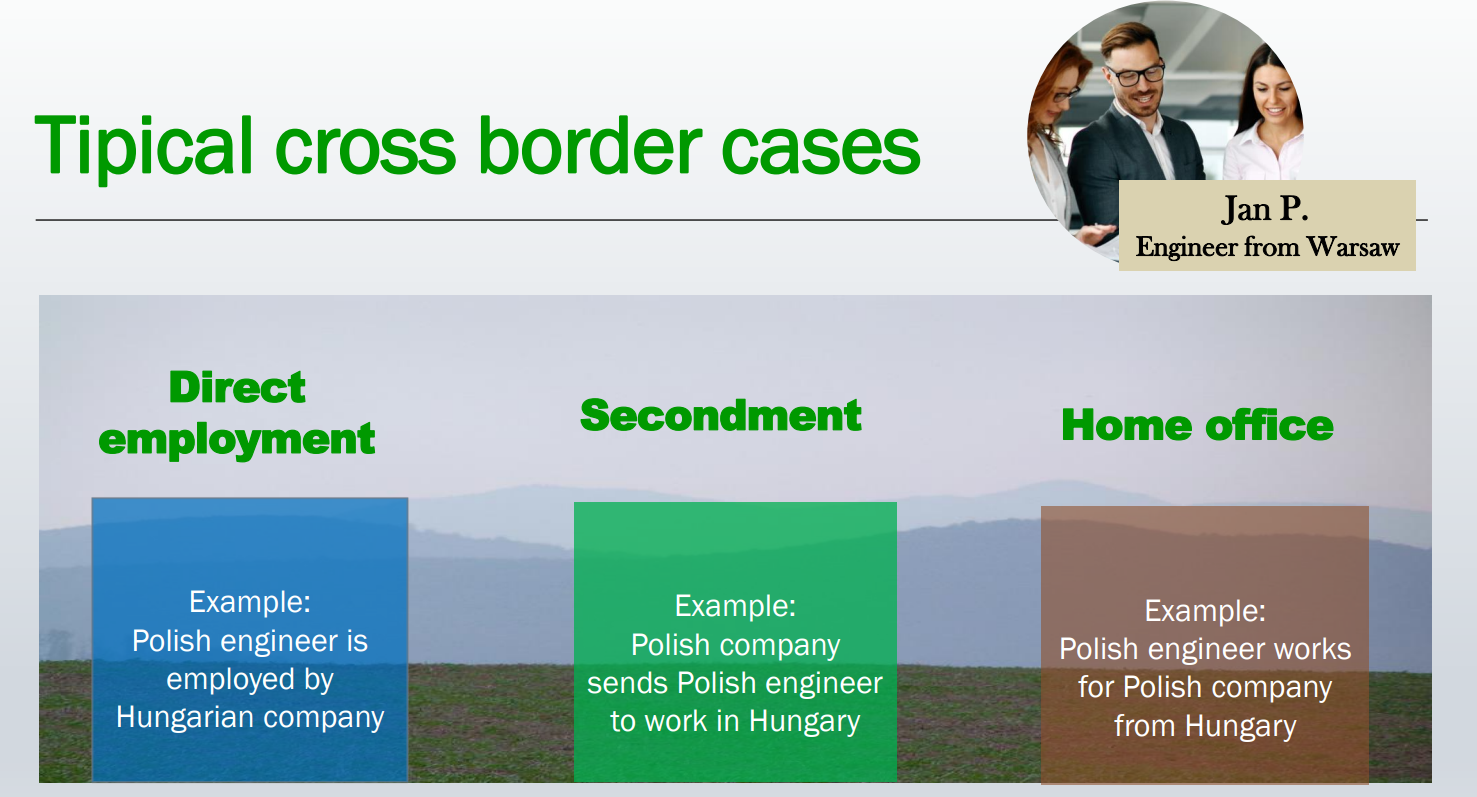

Summary: In this example the Polish engineer is employed by Hungarian company and he works in Hungary. Most typically, the all-over taxability of the engineer will be in Poland if the engineer remains a Polish tax resident. Personal income tax for work income will be due in Hungary, as well as social security.

Aspects to consider:

Two or more employers?

If the engineer normally works as an employee in two or more Member States, this can lead to an incorrect handling of social security by the employer. Employers often disregard the fact that in such cases the engineer will be subject to social security only in the Member State of residence (Poland). This exception from the general rule applies also in the case if a significant part of his activity is carried out in Poland, or if he is employed by different employers whose registered offices are located in other Member States than Poland.

Summary: In this example a Polish company sends a Polish engineer to work at a company in Hungary. Typically, personal income tax for work income will be due in Poland if the engineer spends 183 days or less in Hungary. If he spends more than 183 days in Hungary, then his work income will be taxed in Hungary, however his all-over taxability will be in Poland if the engineer is a Polish tax resident. Social security will be due in Poland.

Aspects to consider:

Summary: In this example the Polish engineer moves to Hungary permanently and carries out distance work for a Polish company from his home in Hungary. In most cases the all-over taxability of the engineer will be in Hungary including personal income tax for work income. Social security will also be due in Hungary.

Aspects to consider:

What about corporate income tax?

This question may seem out of place, however a person working at a home office in Hungary may create corporate income tax liability for the foreign employer. In our example, the Polish company may be deemed to have a “permanent establishment” in Hungary for corporate income tax purposes in a wide set of constellations, such as in the case of visiting and negotiating with customers.

In all cases of cross border employment, whether it is planned by a foreign or a Hungarian company, it necessary to analyse the tax and social security consequences on an individual basis for every employee in advance. The common scenarios described above have been based on an economic relationship between two EU Member States, namely Hungary and Poland. In this respect it is to be noted that the results of our general considerations would have been completely different if we had analysed examples involving a non-EU member country.

Note :This article is based on our presentation at the Hungarian-Polish Chamber of Commerce in February 2023.

Célunk, hogy maradandó értékeket teremtsünk ügyfeleink részére.

Ehhez kiemelkedő minőségű szolgáltatásokkal járulunk hozzá a következő területeken:

Esettanulmányainkban néhány gyakorlati példa segítségével mutatjuk be tevékenységünket és az ügyfeleink számára elért előnyöket:

A member firm of DFK International a worldwide association of independent accounting firms and business advisers

© 2024

© 2024