A nemzetközi cégek körében egyre gyakoribb a határokon átnyúló foglalkoztatás. Ennek jogi és adózási vonzatai összetettek, érdemes előre megtervezni a folyamatok adózási és társadalombiztosítási vonzatát. Az alábbiakban a határon átnyúló foglalkoztatás három leggyakoribb esetét ismertetjük.

Egy Magyarországon dolgozó lengyel mérnök példáját alapul véve elemezzük az adó- és társadalombiztosítási következményeket és lehetőségeket, rávilágítva néhány klasszikus buktatóra is. Bár példánkban a munkavállaló lengyel állampolgár, az elemzés eredménye a más EU-országokból, például Németországból, Ausztriából, Szlovákiából, stb. érkező dolgozók esetében is hasonló. A cikk többi része angolul olvasható az alábbiakban.

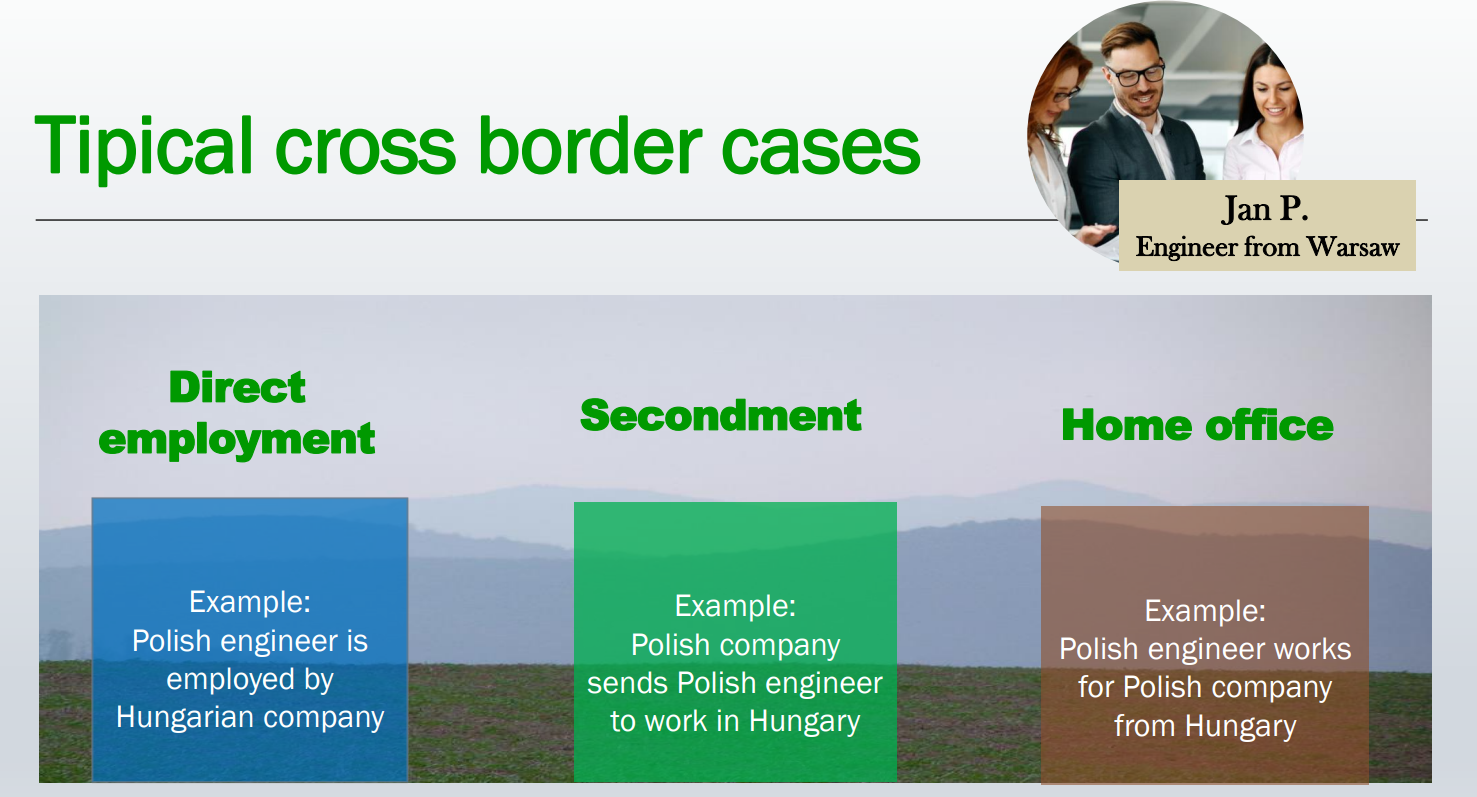

Summary: In this example the Polish engineer is employed by Hungarian company and he works in Hungary. Most typically, the all-over taxability of the engineer will be in Poland if the engineer remains a Polish tax resident. Personal income tax for work income will be due in Hungary, as well as social security.

Aspects to consider:

Two or more employers?

If the engineer normally works as an employee in two or more Member States, this can lead to an incorrect handling of social security by the employer. Employers often disregard the fact that in such cases the engineer will be subject to social security only in the Member State of residence (Poland). This exception from the general rule applies also in the case if a significant part of his activity is carried out in Poland, or if he is employed by different employers whose registered offices are located in other Member States than Poland.

Summary: In this example a Polish company sends a Polish engineer to work at a company in Hungary. Typically, personal income tax for work income will be due in Poland if the engineer spends 183 days or less in Hungary. If he spends more than 183 days in Hungary, then his work income will be taxed in Hungary, however his all-over taxability will be in Poland if the engineer is a Polish tax resident. Social security will be due in Poland.

Aspects to consider:

Summary: In this example the Polish engineer moves to Hungary permanently and carries out distance work for a Polish company from his home in Hungary. In most cases the all-over taxability of the engineer will be in Hungary including personal income tax for work income. Social security will also be due in Hungary.

Aspects to consider:

What about corporate income tax?

This question may seem out of place, however a person working at a home office in Hungary may create corporate income tax liability for the foreign employer. In our example, the Polish company may be deemed to have a “permanent establishment” in Hungary for corporate income tax purposes in a wide set of constellations, such as in the case of visiting and negotiating with customers.

In all cases of cross border employment, whether it is planned by a foreign or a Hungarian company, it necessary to analyse the tax and social security consequences on an individual basis for every employee in advance. The common scenarios described above have been based on an economic relationship between two EU Member States, namely Hungary and Poland. In this respect it is to be noted that the results of our general considerations would have been completely different if we had analysed examples involving a non-EU member country.

Note :This article is based on our presentation at the Hungarian-Polish Chamber of Commerce in February 2023.

Célunk, hogy maradandó értékeket teremtsünk ügyfeleink részére.

Ehhez kiemelkedő minőségű szolgáltatásokkal járulunk hozzá a következő területeken:

Esettanulmányainkban néhány gyakorlati példa segítségével mutatjuk be tevékenységünket és az ügyfeleink számára elért előnyöket:

A member firm of DFK International a worldwide association of independent accounting firms and business advisers

Helyi megoldások

nemzetközi vállalatok

részére

Professzionális tanácsadás.

Elismert vállalatok bizalmával.

Számviteli szolgáltatásaink igazodnak ügyfeleink igényeihez: néhány ügyfelünk tartósan kiszervezi hozzánk könyvelését, míg mások csak ideiglenes számviteli szolgáltatásokat igényelnek, addig, amíg az új cég számviteli részlegét felkészítjük a könyvelés átvételére.

Szolgáltatásunk ezért kiterjed a Magyarországon újonnan alapított leányvállalatok esetében az integrált számviteli rendszerek felépítésében való közreműködésre. Már fennálló számviteli rendszer esetén professzionális szinten vállalunk számviteli tanácsadást, amelyet számos cég elsősorban a működés kezdeti időszakában ítél hasznosnak. Szükség esetén javaslatokat teszünk az IAS, IFRS vagy US-GAAP standardoknak történő megfelelés terén is.

Vállaljuk olyan vállalkozások teljeskörű könyvelését, amelyek ezt nem saját munkavállalóik révén kívánják megoldani. Szolgáltatásunk tartalmazza a beszámolókészítést továbbá az adóbevallások elkészítését is. Ilyen esetekben az anyavállalat integrált rendszeréhez illetve igény esetén a IAS, IFRS vagy US-GAAP standardokhoz illeszkedő számviteli struktúrát alkalmazunk. A folyamatos könyvvezetés során a vállalkozás igényeinek megfelelő formában és gyakorisággal szolgáltatunk információkat. Fontos számunkra a megbízóinkkal történő folyamatos kapcsolattartás és az időközben felmerülő kérdések pontos és gyors megválaszolása.

Teljesen digitális könyvelési platformunk valós idejű hozzáférést biztosít ügyfeleink részére számviteli adataikhoz, biztosítva a pontosságot, átláthatóságot és hatékonyságot.

A teljesen digitális könyvelési rendszer további hasznos funkciója az ügyfeleink igényeire szabott, részletes pénzügyi jelentések készítése. Az egyéni paraméterezés alapján kialakított riportok értékes betekintést biztosítanak a vállalkozás vezetése és tulajdonosai számára a cég számviteli adataiba, jövedelmezőségébe, vagyoni helyzetébe és likviditásába, lehetővé téve a sikeres döntéshozatalt.

A rendszer további fontos előnye az ügyfeleink és könyvelőik közötti hatékony, digitális együttműködés. A platform lehetővé teszi a közvetlen kommunikációt és a dokumentumok megosztását.

Bár a legtöbb magyarországi cég magyar forintban könyvel, ez nem feltétlenül ideális a nemzetközi tevékenységet folytató vállalkozások számára. Szolgáltatásaink keretében vállaljuk a számviteli rendszer devizás könyvelésre, például EUR-ra, USD-re vagy CHF-re történő átállítást és a könyvek devizában történő vezetését outsourcing formájában.

Bérszámfejtési szolgáltatásainkat olyan cégeknek ajánljuk, amelyek számára fontos a fizetések bizalmasságának biztosítása, illetve amelyeknél nem gazdaságos a saját bérszámfejtési részleg kiépítése. Bérszámfejtési szolgáltatásaink magukban foglalják a személyi jövedelemadó, nyugdíj- és egészségbiztosítási alapok, valamint az egyéb járulékok számfejtését és bevallását is.

Ezen szolgáltatásaink címzettjei azok a külföldi vállalkozások, akik Magyarországi tevékenységük folytatásához nem kívánnak központi adminisztratív irodát létrehozni. A székhelyszolgáltatás keretében üzleti címet biztosítunk Budapest központi részén található irodánkban és elvégezzük a kapcsolódó feladatokat, mint például a levelezés továbbítása, adminisztráció ill. iktatás. A székhelyszolgáltatást a könyvelési outsourcing szolgáltatásokat igénybe vevő ügyfeleink részére kínáljuk kiegészítő szolgáltatásként.

© 2025

© 2025