The Hungarian Tax Authority NAV's has formed an Artificial Intelligence Working Group (MIMCS) to conduct future research based on the data assets of the tax office.

The tasks of the working group created in April 2022 include the development of a proposal for a semantic data asset methodology for machine learning. Work will also concern research on algorithms and the development of validation methodologies. Although the research data will be anonymous, data protection rules will be considered as a limit to the operations.

In addition to the findings of artificial intelligence, information provided by taxpayers in the form of filings, there is a constant influx of data into the electronic systems of the Tax Authority also from third parties. Below we examine these sources of information and the legal grounds that they are based upon.

Certain third parties are obliged to provide tax information to the Hungarian Tax Authority automatically or upon request by law. These include banks and insurances which need to fulfill reporting requirements. Contracting parties under civil law are also required to provide tax relevant information. In addition there is a system of exchange of tax information with foreign tax authorities in the European Union and in other states.

VAT-related filings, such as VAT-returns or Intrastat are an important source of information for tax authorities world-wide. In Hungary the Tax Authority NAV has direct access to invoices issued by taxpayers, because, as based on specific rules, the content of invoices including VAT must electronically be transmitted to the Tax Authority upon issuance. Also, the movement of goods by transportation in Hungary is monitored by a digital system called EKAER, where companies must declare the precise route of goods delivered. While the system was initially designed to prevent VAT fraud, it contains a plethora of information that the Tax Authority can use in tax audits. As of 1st January 2021, only those products must be reported for EKAER, which are listed in the Schedule to the Decree 51/2014 (Dec 31) of the Minister for the National Economy on the determination of risky products in association with the operation of the Electronic Public Road Transportation Control System.

The Tax Authority also has the possibility to obtain information from other state or private digital databases, such as systems in the private economy containing customer information. Many of these systems are accessed by customers on the internet. Typical examples are hotel reservations and other booking platforms, credit card and similar payment systems, even computer games. The availability of information is not restricted to Hungarian providers, but it can be also obtained within the framework of international cooperation between the Tax Authority in Hungary and tax authorities abroad.

A network of international tax treaties, mostly on a bilateral but also on a multilateral basis make it possible for tax authorities to exchange tax information with states not just inside, but also outside of the European Union. The most extensive regulations in this respect, however, have been implemented in Hungary based on the directives of the European Union.

For example, a Hungarian company not reporting its related companies and not documenting its transfer pricing transactions will easily be detected. The transparency of the system can also be illustrated by a Swedish investor investing in several apartments in Budapest and renting them out through Airbnb. In this case, the Hungarian and the Swedish Tax Authorities will have total transparency on the income of the Swedish individual, because Airbnb as an Irish company is obliged to supply information to the Irish Revenue which will be shared with the other two related tax authorities.

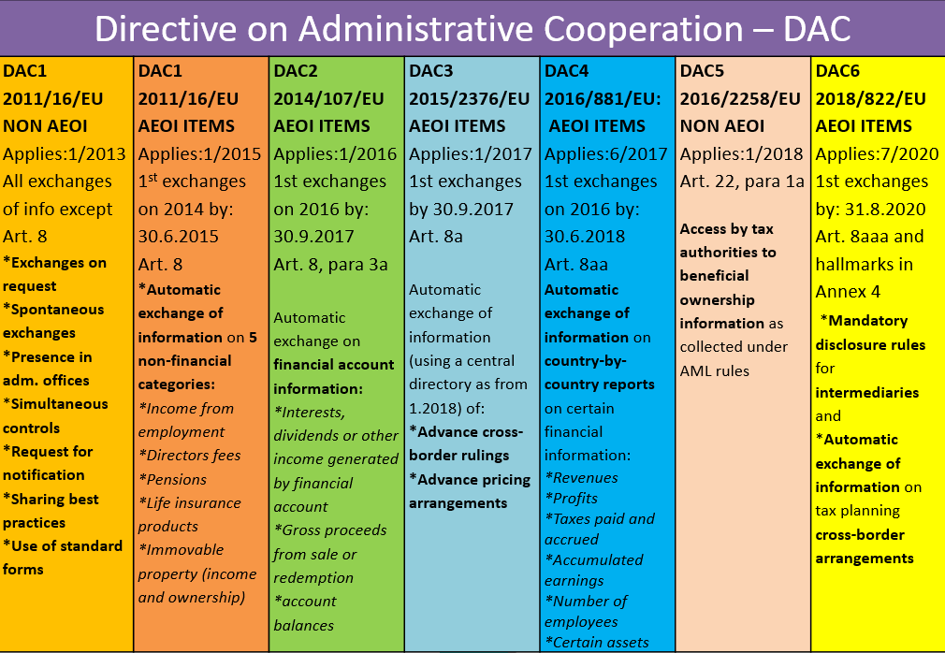

The exchange of information in tax matters within the European Union was introduced in 2013 by Council Directive 2011/16/EU. The Directive provides for mandatory exchange of five categories of income and assets:

The scope has later been extended to

These latter forms of information exchange apply not just in the European Union. They have been introduced in many other jurisdictions as well, as based on the international standard of the OECD. However, the exchange of tax information in the EU goes further than in the OECD, providing also for a practical framework to exchange information - i.e. standard forms for exchanging information on request and spontaneously, as well as computerised formats for the automatic exchange of information. The EU has implemented secured electronic channels for the exchange of information and a central directory for storing and sharing information on cross-border tax rulings, advance pricing arrangements and tax planning schemes.

The table below indicates the steps by which today’s extensive exchange of tax information in the EU has been developed.

Source: European Commission

The broad exchange of information on taxpayers raises the question if data protection principles are respected at all times, with special attention to the rules of the GDPR. This aspect of tax information exchange has been the subject of several court decisions in the European Union.

The issue that the courts have examined is the legal grounds for handling personal data and if the process entailed any breaches of privacy through the tax authorities. These cases are increasingly complex, but it can generally be stated that privacy is a fundamental right of the taxpayer and any limitations to it, such as information exchange between tax authorities, must be proportionate and necessary to protect the general interest.

Wir sind bestrebt, zum Wertschöpfungsprozess unserer Mandanten beizutragen, indem wir ihre Ziele verstehen und sie dabei unterstützen, diese zu erreichen.

In unseren Fallstudien veranschaulichen wir anhand einiger Beispiele, wie wir uns für unsere Auftraggeber täglich einsetzen und welche Vorteile wir für sie erzielen.

A member firm of DFK International a worldwide association of independent accounting firms and business advisers

Lokale Lösungen,

internationale

Expertise

Kompetenz, der Unternehmen vertrauen.

Erfahrung, die überzeugt.

Unsere Buchführungsleistungen sind exakt auf die Bedürfnisse unserer Mandanten zugeschnitten. Viele unserer Mandanten haben ihre ungarische Buchhaltung und Bilanzierung dauerhaft an uns ausgelagert, um von einer effizienten und professionellen Abwicklung zu profitieren. Andere Unternehmen nutzen unsere Unterstützung nur vorübergehend, bis ihr internes Team vollständig geschult ist und die ungarische Finanzbuchhaltung eigenständig übernehmen kann.

Als beratungsorientierte Wirtschaftskanzlei bieten wir weit mehr als klassische Treuhandservices. Wir arbeiten mit einer etablierten, vollständig digitalen Buchhaltungsplattform eines renommierten Herstellers, die in Deutschland, Österreich und der Schweiz erfolgreich im Einsatz ist. Wir übernehmen den gesamten Buchführungs-, Bilanzierungs- und Reporting-Prozess und liefern regelmäßige, präzise Reports im gewünschten Dateiformat, darunter Excel, CSV oder XML. Für zahlreiche Mandanten optimieren wir den Workflow, indem wir die Daten direkt in ihr ERP-System hochladen, sodass sie jederzeit aktuelle Finanzinformationen abrufen können.

Eine enge, transparente Kommunikation ist für uns essenziell. Unsere erfahrenen Experten stehen Ihnen regelmäßig zur Verfügung – auf Wunsch auch in englischer Sprache. So gewährleisten wir eine reibungslose Zusammenarbeit und eine Buchhaltung, die sich nahtlos in Ihre Geschäftsprozesse integriert.

Unsere vollständig digitalisierte Buchhaltungsplattform optimiert das Finanzmanagement für Unternehmen jeder Größe. Dank eines cloudbasierten Systems erhalten unsere Mandanten in Echtzeit Zugriff auf ihre Buchhaltungsdaten, wodurch höchste Genauigkeit, Transparenz und Effizienz gewährleistet werden. Zudem sorgt die nahtlose Integration von Steuer-Compliance-Funktionen dafür, dass unsere Steuerberater die gesetzlichen Anforderungen unserer Mandanten mittels digitaler Daten direkt aus der Buchhaltung erfüllen können.

Ein weiterer Vorteil unserer digitalen Buchhaltungsplattform ist die Möglichkeit, detaillierte Finanzberichte nach individuellen Anforderungen abzurufen. Diese Berichte bieten wertvolle Einblicke in Cashflow, Rentabilität und die finanzielle Gesamtsituation und unterstützen fundierte Geschäftsentscheidungen.

Darüber hinaus ermöglicht die Plattform eine flexible und digitale Zusammenarbeit zwischen unseren Mandanten und ihren Buchhaltern. Durch eine zentrale Lösung für Dokumentenaustausch und direkte Kommunikation mit unseren Buchhaltungsexperten wird die Effizienz der Arbeitsabläufe erheblich gesteigert. Ob Lohnbuchhaltung, Steuererklärungen oder Finanzplanung – unsere Mandanten profitieren von einer sicheren, zuverlässigen und skalierbaren Buchhaltungslösung, die exakt auf ihre Bedürfnisse zugeschnitten ist.

Während die meisten Unternehmen in Ungarn ihre Bücher in ungarischen Forint führen, kann dies für viele international tätige Unternehmen ein klarer Nachteil sein. Wir beraten Sie gerne zur Optimierung Ihrer Buchhaltungswährung und stellen Ihr Buchhaltungssystem von HUF auf die funktionale Währung Ihrer Wahl um, sei es EUR, USD, CHF oder eine andere Währung.

Wir bei Gyarmathy&Partners unterstützen Sie beim Aufbau von integrierten Rechnungslegungs- und Berichterstattungssystemen für Ihr ungarisches Tochterunternehmen. Wenn Sie ein bereits vorhandenes Programm ihrer Unternehmensgruppe auch in Ungarn zur Finanzbuchhaltung, Bilanzierung, bzw. zum Reporting verwenden möchten, helfen wir Ihnen, Ihre Software an die ungarischen Standards anzupassen.

Wir beraten Sie gerne bei allen Fragen zu den Besonderheiten des ungarischen Bilanzwesens, wie z.B. die Kalkulationen von EBIT und Dividenden, sowie zur Anwendung von IFRS und US-GAAP.

Wenn Ihnen die Einrichtung einer eigenen Lohnbuchhaltung für Ihr Unternehmen nicht rentabel erscheint und Ihnen absolute Vertraulichkeit bei der Lohn- und Gehaltsabrechnung wichtig ist, übernehmen wir gerne sämtliche Lohnabrechnungsaufgaben für Sie. Dies ist eine große administrative Entlastung sowohl für kleinere Tochtergesellschaften als auch für größere Unternehmen, die zur Auszahlung von Sozialversicherungs- und Mutterschaftsgeldern verpflichtet sind. Unsere Experten erfüllen die besonderen gesetzlichen Anforderungen an Lohnbuchhalter von Unternehmen mit mehr als 100 Mitarbeitern.

Während wir uns um Ihre gesamte Lohnbuchhaltung kümmern, kann sich Ihr Unternehmen auf Ihr Kerngeschäft konzentrieren. Zusätzlich zum regelmäßigen Reporting liefern wir eine monatliche E-Banking-Datei für die Zahlung von Gehältern, Steuern und Sozialversicherungsbeiträgen. So erledigen Sie die Überweisung von Löhnen und Steuern mit wenigen Klicks in Ihrem E-Banking-System.

Unsere Dienstleistungen umfassen die Erledigung sämtlicher lohnbezogenen Steuererklärungen, Meldungen an die Renten- und Krankenkassen sowie anderer obligatorischer staatlicher Abgaben. Die meisten unserer Mandanten, die ihre Buchhaltung und Berichterstattung an uns auslagern, beauftragen uns auch mit der Lohnbuchhaltung.

Als Arbeitgeber können Sie die zu erwartenden Lohnkosten mithilfe unseres Gehaltsrechners vorauskalkulieren und einschätzen.

Unsere Firmensitz-Dienstleistungen richten sich speziell an Unternehmen, die in Ungarn keinen eigenen Hauptsitz benötigen. Wir bieten Ihnen einen offiziellen Firmensitz im Stadtzentrum von Budapest und übernehmen die mit der Firmengründung und dem Geschäftsbetrieb des Unternehmens verbundenen administrativen und Backoffice-Aufgaben.

Selbstverständlich erledigen wir Ihnen gerne die Eintragung des neuen Firmensitzes ins Handelsregister oder die gesamte Handelsregistereintragung im Falle einer neuen Firmengründung in Ungarn. Diese Dienstleistungen richten sich als ergänzender Service an Mandanten, die unsere Outsourcing Buchhaltungs- und Steuerberatungsleistungen in Anspruch nehmen.

© 2025

© 2025